Heat Pump Financing: A Practical Guide for Homeowners

Discover practical heat pump financing options, compare loan types, incentives, and strategies to maximize energy savings while minimizing upfront costs for homeowners, builders, and managers.

Heat pump financing makes efficient heating affordable by spreading upfront costs across loans, rebates, and payback programs. According to Heatpump Smart, the best approach blends low-interest loans, energy-efficiency incentives, and utility programs to reduce both monthly payments and total costs.

Why heat pump financing matters for homeowners

Heat pump financing is more than a payment plan—it's a pathway to lower energy costs and improved comfort. According to Heatpump Smart, upfront costs can be a barrier to adopting energy-efficient heating, but thoughtful financing changes that equation. By pairing financing with incentives and utility programs, homeowners, builders, and property managers can start saving on energy bills sooner while spreading payments over time. This section lays the groundwork by explaining how different funding channels interact with your home’s utility use, local climate, and occupancy patterns. You will learn how to estimate the long-term benefit of a heat pump beyond the sticker price, including reduced maintenance, longer equipment life, and resilience during peak-demand periods.

Financing options tailored to your situation

Options for heat pump financing vary by location and lender, but most projects benefit from a blended approach. Traditional loans offer predictable monthly payments, while PACE programs can cover a larger portion of the installation by tying repayments to property taxes (where eligible). Manufacturer or retailer financing can provide introductory rates or bundled maintenance plans. Utility rebates and state or federal incentives can further reduce effective cost. Heatpump Smart's analysis suggests starting with a formal cost-benefit assessment, then mapping out the best mix of loan terms, rebates, and low-interest offerings to fit cash flow and ROI targets.

Evaluating lenders and incentives: what to compare

When shopping for heat pump financing, compare total cost of ownership, not just the monthly payment. Look at interest rates, origination fees, prepayment penalties, and whether incentives stack with other programs. Some lenders offer deferred payments during the first year, or lower rates for high-efficiency models certified by Energy Star. Heatpump Smart notes that the strongest options combine rebates with favorable loan terms to shorten the payback period and maximize lifetime savings. Don’t neglect service and warranty packages—these can influence annual costs and reliability.

How incentives and rebates affect the total cost

Incentives and rebates directly reduce upfront or ongoing costs, improving your ROI. When you qualify for multiple programs (rebates, tax credits, and utility discounts), you should recalculate your net installed cost and monthly payment accordingly. The cumulative effect of incentives can turn a mid-range model into a near-term budget win. Heatpump Smart’s framework emphasizes documenting all eligible programs before finalizing a purchase, and coordinating with your installer to ensure you meet energy-efficiency criteria.

Step-by-step financing roadmap for a retrofit

- Define project scope and budget. 2) Gather energy-use data and model expected savings. 3) Identify eligible financing options and incentives. 4) Run loan scenarios across term lengths and down payments. 5) Apply for rebates and incentives in parallel with loan approval. 6) Close the deal and monitor performance with an energy-tracking plan. Heatpump Smart recommends using a project-specific ROI calculator to compare scenarios and confirm affordability.

Common pitfalls and how to avoid them

Avoid extending debt beyond the expected payback window. Don’t assume incentives will be permanent or stack automatically. Read the fine print on loan fees, termination clauses, and warranty coverage. Also be wary of pushy sales tactics that push high-cost configurations; instead, demand transparent quotes and a clear breakdown of each program’s impact on your bottom line.

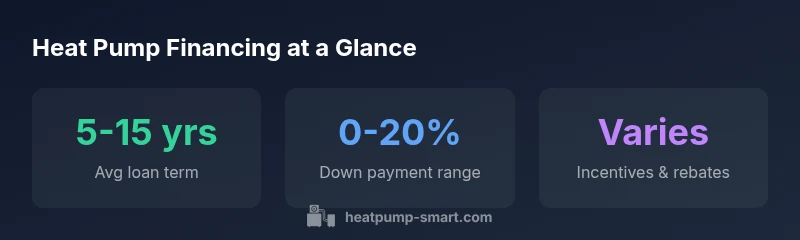

Common heat pump financing channels

| Funding Channel | Key Benefit | Typical Range (qualitative) | Eligibility Notes |

|---|---|---|---|

| Loan financing | Low monthly payments | 5-15 years | Credit requirements vary |

| PACE programs | No upfront costs via property tax assessment | Flexible terms | Property value and location matter |

| Manufacturer/utility incentives | Direct rebates or lower effective APR | Varies by program | Must meet energy efficiency criteria |

Your Questions Answered

What is heat pump financing?

Heat pump financing refers to loans, leases, or incentives used to cover upfront costs of purchasing and installing a heat pump. It helps spread payments over time while aiming to reduce energy bills.

Heat pump financing lets you spread the cost over time, so you can start saving sooner.

What financing options are typically available for heat pumps?

Common options include traditional loans, home equity lines of credit, PACE programs where eligible, and manufacturer or utility rebates that reduce the net cost.

You can choose from loans, HELOC, PACE programs, and rebates.

Do rebates and tax credits affect financing terms?

Yes, rebates reduce upfront cost and can improve loan-to-value, sometimes lowering interest or enabling shorter payback. Tax credits are claimed separately on your return.

Rebates cut upfront costs and may improve terms.

Is PACE financing available for rental properties?

PACE is sometimes available for eligible properties, but rules vary by state and lender. Property owners should verify eligibility and transfer responsibilities.

PACE for rentals depends on where you are; check local programs.

How do I estimate monthly payments for heat pump financing?

Use the loan amount, interest rate, and term to estimate monthly payments; many lenders provide calculators and Heatpump Smart also offers framework.

Use a loan calculator with your amount, rate, and term.

What are common mistakes to avoid when financing a heat pump?

Avoid over-leveraging, ignoring incentives, and selecting a plan with high fees. Ensure you understand terms and total cost.

Don’t overextend and read the fine print.

“Financing is not just borrowing; it's a strategy to maximize energy savings over the life of your heat pump.”

Top Takeaways

- Define your budget before shopping financing.

- Prioritize programs that combine rebates with low-interest loans.

- Compare total cost over the loan lifetime, not just monthly payment.

- Check eligibility for PACE, utility incentives, and tax credits.

- Work with a lender who understands heat pump projects.