Heat Pump 0 Finance: How 0% Financing Works for Homeowners

Discover how heat pump 0 finance programs work, where to find 0% financing, eligibility, and how to combine promotions with rebates to significantly lower upfront costs for heat pump installations.

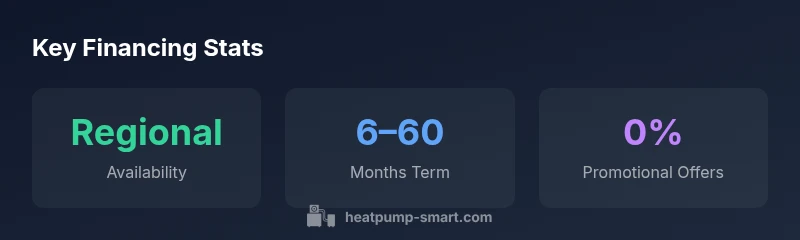

0% financing options for heat pump installations exist but are regionally limited and program-specific. Availability depends on local utilities, manufacturers, and government incentives, with terms commonly ranging from 6 to 60 months for creditworthy applicants. Always compare total repayment, fees, and whether rebates can be stacked with the financing. Consult your installer for current promos.

Understanding 0% financing for heat pumps

0% financing for heat pump installations is not a universal standard; it is a promotional option offered by utilities, manufacturers, or government programs. These programs aim to reduce upfront cost and accelerate adoption of efficient heating. According to Heatpump Smart analysis, the availability of 0% financing varies widely by region and by the specific product and service package. In some markets, a utility may offer 0% financing for equipment purchase and installation bundled with an energy audit or home assessment. In others, manufacturer's promotions may apply only to certain models or to customers who sign up for a financing plan through a preferred lender. It’s essential to read the terms carefully, because even when the rate is 0%, there can be required fees, minimum purchase amounts, or restrictions that affect the true value of the offer.

Where to find 0% financing programs

Promotional financing for heat pumps tends to appear through three main channels: utility programs, manufacturer promos, and government or local energy-efficiency initiatives. Utilities may offer 0% financing as part of an energy-efficiency bundle or rebate-eligibility requirement. Manufacturers sometimes run time-limited offers tied to specific models or installation packages. Government programs can provide low- or no-interest loans with regional eligibility criteria. A practical strategy is to check your utility’s website, contact local HVAC contractors who regularly work with promos, and search state or provincial energy portals. Heatpump Smart notes that program availability evolves, so it’s worth rechecking quarterly.

Eligibility and typical terms

Financing eligibility generally depends on creditworthiness and program-specific criteria, such as occupancy status, installation scope, and whether you qualify for an energy audit. Terms, when offered, commonly range from several months up to five years, with 0% interest for the promo period. There may be minimum purchase thresholds, processing fees, or required maintenance plans. Always ask for a clear payoff schedule and whether any subsequent financing or promotional rates kick in after the 0% window ends. Heatpump Smart emphasizes comparing the total cost of financing versus paying upfront, factoring in any rebates or tax credits.

How financing interacts with rebates and tax credits

Financing can be a powerful tool when paired with rebates and tax incentives. Rebates reduce the upfront price, while tax credits or deductions may apply after installation. When a 0% promo is involved, the effective savings depend on the timing of rebates and whether the lender allows rebates to be deducted from the financed amount. It’s crucial to document all incentives and verify whether the financing terms remain unchanged if you receive a rebate later. In some cases, financing may be used to cover ancillary costs (like ductwork or insulation) that improve overall system performance, amplifying long-term energy savings. Heatpump Smart recommends coordinating with an installer who can map financing with available rebates for a transparent, optimized savings plan.

Practical steps to secure 0% financing

- Get multiple quotes from qualified installers and ask specifically about 0% financing offers. 2) Check your utility and manufacturer promo calendars for current promotions. 3) Gather documents: proof of ownership, recent energy bills, installation scope, and credit information. 4) Read the fine print on any 0% offer—confirm eligibility, what happens when the promo ends, and any fees. 5) Compare offers side-by-side using a simple cost calculator that includes rebates and potential tax credits. 6) If possible, bundle the heat pump with related energy-efficiency upgrades to maximize total savings. Heatpump Smart suggests documenting all incentives and running a final cost-benefit analysis before committing.

Regional considerations and caveats

Regional program availability means what works in one city may not exist in another. Some areas offer robust 0% financing through utilities, while others have none. Market maturity, local incentives, and the presence of participating lenders shape the landscape. Additionally, qualify-for-newsletters and promotional periods can shift with policy changes. Homeowners should keep a flexible plan: monitor local programs, coordinate with installers, and align financing with rebates for the best total value. Heatpump Smart recommends seeking professional guidance to understand the current regional landscape and avoid outdated assumptions.

Comparison of common 0% financing program types for heat pump installations

| Program Type | Terms | Eligibility | Notes |

|---|---|---|---|

| Utility-based 0% financing | Typically 6–60 months | Creditworthy applicants; region-dependent | Check for stacking with rebates |

| Manufacturer promos | Often limited-time offers | Credit requirements; model-specific | Subject to regional availability |

Your Questions Answered

What exactly is heat pump 0 financing?

0 financing is a promotional option offering no-interest for a period but does not eliminate the principal. Always verify terms, end dates, and any fees with your lender.

0 financing is a promotional no-interest period; read the terms and end dates carefully.

Which programs offer 0% financing for heat pumps?

Utility programs, manufacturer promotions, and government energy-efficiency initiatives commonly offer 0% financing. Availability is regional and model-dependent.

Look for utility or manufacturer promos in your area.

How do rebates and tax credits interact with 0% financing?

Rebates lower upfront costs; tax credits may apply after installation. Financing may affect eligibility or the perceived value, so map incentives before signing.

Rebates lower upfront costs; tax credits apply later; plan with your installer.

What should I prepare before applying?

Proof of ownership, a recent energy assessment, detailed quotes, and credit information help streamline the approval process. Have questions ready for the lender.

Gather ownership proof, quotes, and your credit info.

Are there risks with 0% financing?

Promotions can end, raising rates afterward. Ensure you can meet payments if a promo expires and read cancellation or payoff terms.

Watch for promo end dates and long-term payment terms.

Does 0% financing apply to new builds?

Financing for new construction may differ; consult your installer about available programs and whether heat pumps qualify with new-build packages.

Check if new-build programs apply to your project.

“0% financing can reduce upfront costs for heat pumps, but you must compare total payback and program terms to maximize value.”

Top Takeaways

- Check local 0% financing programs first

- Stack financing with rebates for bigger savings

- Read terms carefully and watch for promo end dates

- Prepare documents ahead of applying